Right now [June 2022], markets are experiencing volatility over concerns that recession is headed our way.

The textbook definition of a recession is two consecutive quarters of a decline in US gross domestic product, otherwise known as GDP. Recession is a normal and unavoidable part of any business cycle. But how shallow or severe recession becomes generally determines the effects that it will have on us all.

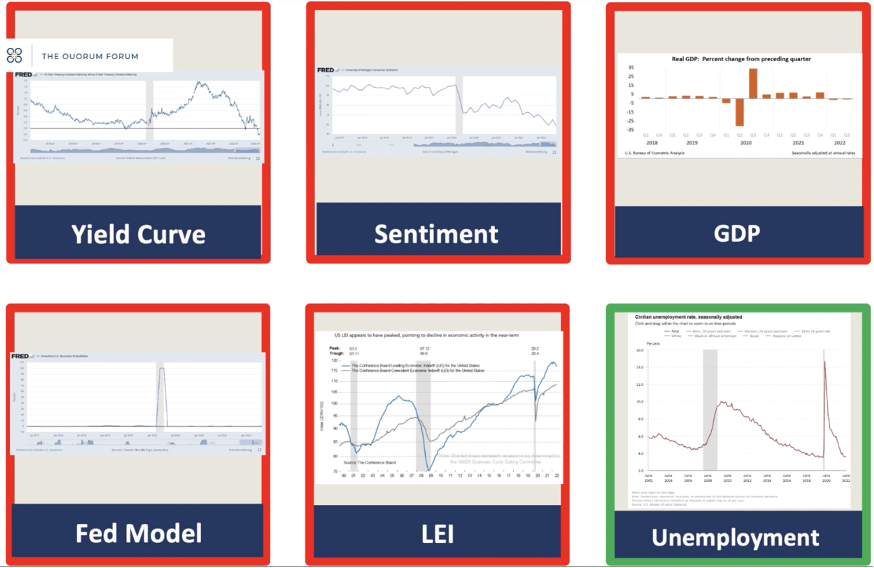

At Quorum, we look at six different indicators to determine the likelihood of a recession happening. We'd like to share those with you now.

- First, we look at the yield curve inversion. Now, a normal yield curve would show short term US Treasury bonds with lower yields than long term US Treasury bonds. This indicator was flashing red back in April [2022] and then again today on June 10 [2022]. We saw an inversion of the yield curve with yields on five-year Treasury bonds posting higher yields than 30-year Treasury bonds.

- The second indicator we look at is consumer sentiment. This indicates how people are feeling about their financial stability. Inflation and war have had sentiment trending negative for a while, and even though there's been a slight improvement recently, as you see on this chart [middle top on the chart below], we consider this indicator to be flashing red, predicting a possible recession.

- The third indicator is GDP growth or decline. The first quarter of 2022 showed a posting of gross domestic product declining 1.5%. So, this is flashing red. And we'll be looking for the second quarter results after the end of June to see if the textbook definition of a recession is validated with another negative quarter of GDP growth. Or, if GDP can pull out a positive performance, perhaps we will avoid a recession.

- The fourth indicator we look at is the Fed model. Now, the New York Fed monitors the probability of a recession by looking at things such as building permits, productivity, and consumption data. This is currently flashing green, showing that a recession is not probable for the next 12 months.

- The fifth indicator is leading economic indicators. This is flashing green. LTI is pointing towards moderate growth in the US economy, despite inflation and other crisis around the globe.

- The sixth indicator is unemployment, and this is flashing bright green. We're at 3.6% unemployment in this country right now. And that's despite the highest number of people resigning from their jobs that we've ever seen in U.S. history.

So, is a recession coming? Our indicators are split 50/50. The stock and bond markets are leaning towards the affirmative with recent declines. And in July we'll see the second quarter GDP report—if it's negative, then we'll have confirmation of a recession. And even if it's positive, we feel that the market will remain volatile for the remainder of 2022.

But there is a silver lining. Historically, recessions clear market excesses and set the stage for formidable returns for patient investors. We continue to keep a long-term view and we will stay diversified. We avoid market timing and will always stick with high quality investments.

Back in June [2022] on this program, we asked the question: “Are we in a recession?”, and we reviewed with you six economic indicators that we follow here a Quorum to gauge whether or not the economy is headed into a downturn.

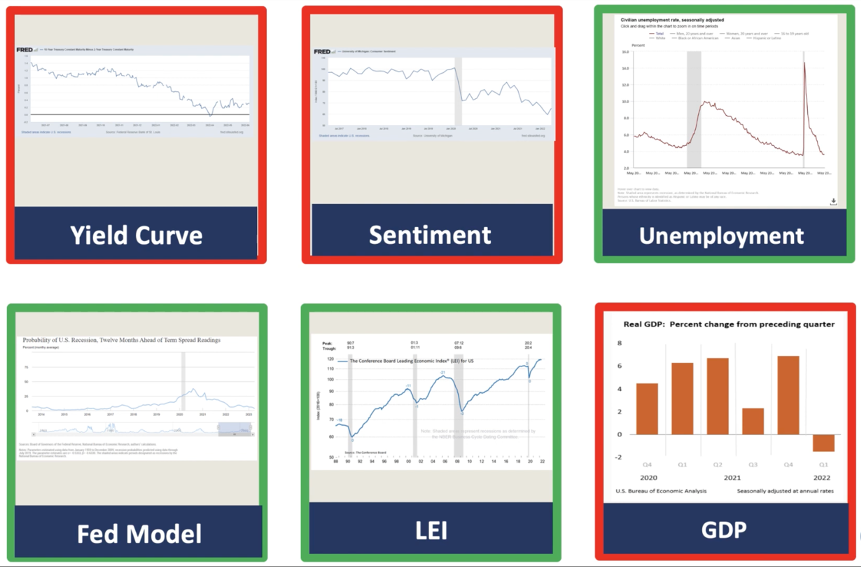

At that time [June 2022], our indicators were split with half showing positive economic data and half showing negative signs in the economy. Today, in early August [2022], our indicators now show five of the six indicators are in the negative camp, with the only exception being unemployment, which is continuing to hold at under 4%.

Additionally, on July 28, it was revealed that gross domestic product for the second quarter posted a negative 0.9%, which marked two consecutive quarters in a row that the US economy shrank. Historically, this has served as a confirmation that the country is experiencing a recession.

But hey, not so fast with that assumption. The word from the Federal Reserve and the White House is that it's different this time. And the discussion amongst economists and Wall Street pundits offers mixed opinions on whether or not this is credible measurement.

On the one hand, recession has never occurred with unemployment at a remarkably low level like it is today. And, second quarter corporate earnings came in with 70% of companies meeting or exceeding profit forecasts.

But on the other hand, it's hard to argue that the economy is growing when inflation is eroding 8-9% of the consumers purchasing power coinciding with a confirmation that GDP went backwards during the first six months of the year.

Here's something to think about.

Historically, the stock market has been an efficient barometer of predicting what economic activity will be about six months into the future. In economic terms. This is referred to as a discounting mechanism.

Simply put, no investor would buy a stock that they didn't believe would be more valuable tomorrow. Then, consider what markets did so far in 2022. Stock indices hit new all-time highs during the first week of January and then proceeded to consistently pull back to the point that, by mid-June [2022], the S&P 500 was down more than 20% and the NASDAQ was down nearly 30%.

And while we were in a bear market with looming fears of recession, that coincidentally is the same six-month period where GDP turned negative for two consecutive quarters, even though GDP had been forecasted to be positive for both of those periods.

It's arguable that the market predicted what few others saw coming. Our belief is that we're probably in a shallow recession. What is unknown is: Will we slip into a steeper decline from here or see the economy smooth out some of the imbalances that caused GDP to erode in the first place?

Ultimately, the outcome seems dependent on how well the Federal Reserve executes on rate policy while systematically reining inflation back down to the target range that they have of 2-2.5%. I've never given much credence to the phrase “it's different this time”, especially when the argument goes against historical precedent.

And ultimately, we will not know if a recession is official until it is confirmed and reported by the National Bureau of Economic Research, otherwise known as NBER. NBER is a private, nonpartisan, highly-credible think tank of economists from top universities around the country. They alone have the final say, on what were the dates that the U.S. enters into a recession and then recovered back out of that recession.

The irony here is that NBER typically issues their findings anywhere between nine months to two years after a recession has begun. In other words, the economy would likely be well on its way back into a recovery by the time the official word on any recession is confirmed. If you wait for that confirmation, you will likely miss any opportunities that were created by a downturn.

Our best advice? Follow a disciplined approach and keep a long-term perspective. Simple as that.