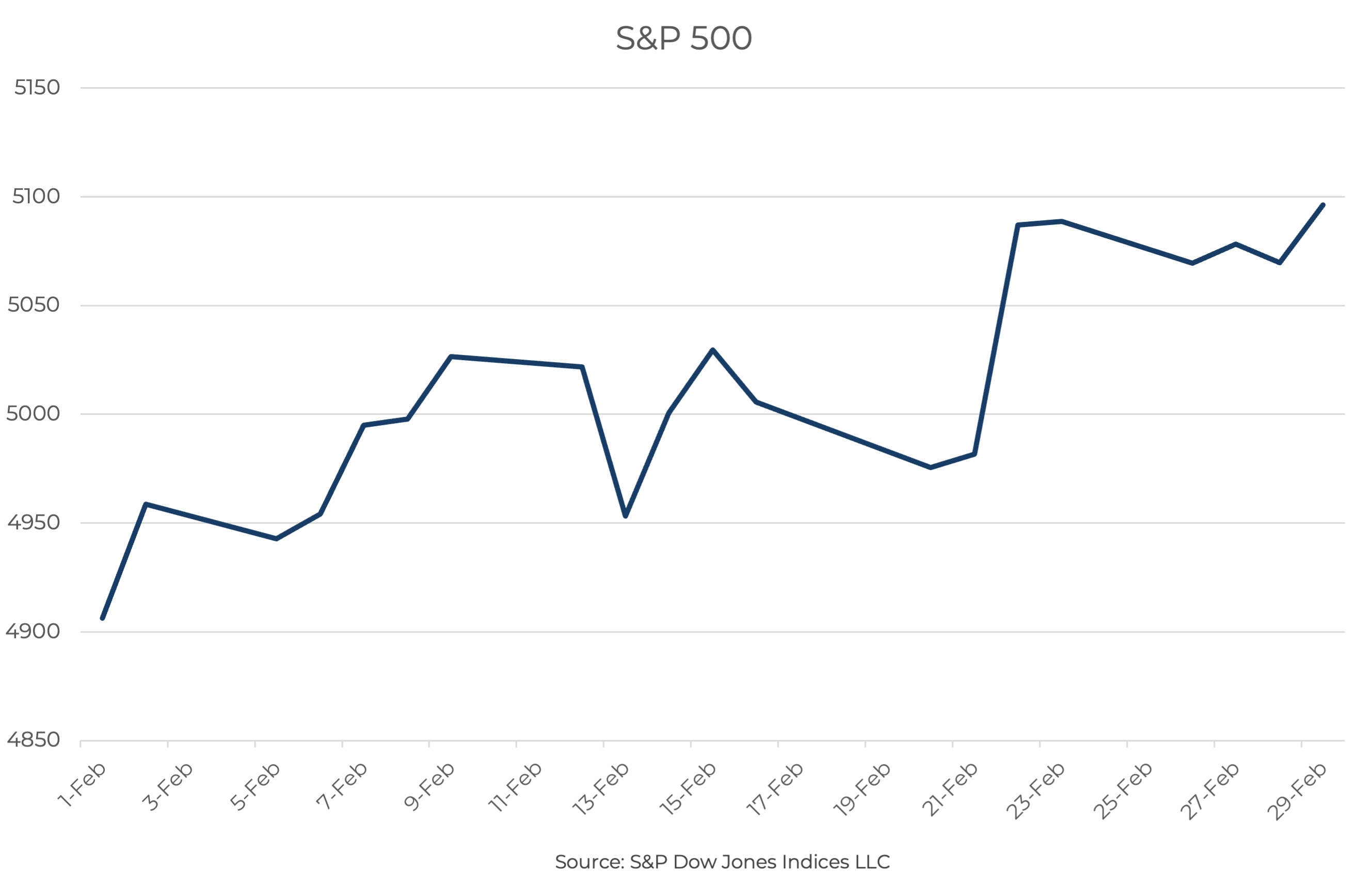

February saw the S&P 500’s first break through the 5,000 ceiling, and there were eight new closing highs during the month.

A strong equity market is welcome, but how will it impact the rest of the economy? With interest rates high and inflation still on the way down but not hitting the target, the cost of everything has increased. And if you’ve been looking to buy a home, you may have been stymied either by the low housing inventory or the high cost of a mortgage. Will the economy start to come into balance this year? Or are we still at risk of a slowdown as Federal Reserve Chairman Powell waits to see inflation come down definitively, while high rates stifle growth?

The Fed is focused on bringing down inflation, but to do so they need to parse data from the economy as a whole. The decision on when to cut rates is arguably more momentous than normal, as it signals the end of the fight. That perception could fire up the economy and result in inflation spiking again. All along, Powell has been cautious and articulated that the Fed would not hesitate to go back to a tightening stance if it was warranted. However, it’s easier to get the timing right the first time. Markets have gone from expecting a March cut, to waiting for a June cut.

In testimony to Congress, Powell again made mention that the risk of “Reducing policy restraint to soon or too much could result in a reversal of progress…and require tighter policy to get inflation back to 2%.”

However, Powell was clear that the risks have become more balanced, and that the Fed “can and will begin” to cut rates this year.

Let’s get into the data:

· CPI was still over 3%. CPI rose 3.1% for the 12 months through January. Core CPI, excluding food and energy, rose 3.9%, the same as in December

· Consumer spending faltered. January retail sales, as reported by the Commerce Department, fell 0.8% from December.

· Businesses saw progress on prices. The S&P 500 Global Flash US Composite PMI fell from 52.0 to 51.4 in mid-February, signaling a marginal expansion in business activity

· Houses are still expensive. Mortgage rates ended the month below 7% after spiking during February. But home prices were up 5% from the prior year, according to RedFin

What Does the Data Add Up To?

Businesses are beginning to be happy, the market is anticipating cuts, and earnings season has seen progress. Inflation has hit a hiccup, but the consumer appears to have taken the foot off the gas, which could create more downward movement. Housing is an ongoing problem. If rates come down, it may make houses even more expensive as more participants enter the bidding fray.

Vice-chair Philip Jefferson, in his first speech, discussed the remaining risks to the economy that the Fed is concerned about. The three key risks are as follows, in the Fed’s order:

· The Fed sees the consumer as key in the fight against inflation, and if consumer spending is more resilient than they are currently expecting, “progress on inflation could stall”

· Employment needs to fall for the economy to come into balance with inflation at the target rate of 2%, but the Fed is concerned that employment may weaken too much.

· Geopolitical risks remain a wild card.

The Fed meets on March 20th, and the markets will be looking for more guidance on what to expect. Once we get beyond the decision to cut rates, the next issue is the pace of rate cuts, and whether the Fed will hit their expected target rate this year – or revise it.

Equity Markets in February

· The S&P 500 was up 5.17%

· The Dow Jones Industrial Average rose 2.22%

· The S&P MidCap 400 gained 5.80%

· The S&P SmallCap 600 was up 3.15%

Source: S&P Global. All performance as of February 29, 2024

February saw all eleven sectors post gains, with Consumer Discretionary out front with an 8.60% return for the month. Utilities did worst, barely eking out a positive return with 0.53%. The S&P 500 saw gains on 13 of 20 trading days over the month, and while the Magnificent 7 still dominate, there was a clear leader. On the last day of the month, a deal was reached on a stop-gap budget, relieving some of the possible clouds over potential performance in March.

Bond Markets

The 10-year U.S. Treasury ended the month at a yield of 4.26%, up from 3.93% the prior month. The 30-year U.S. Treasury ended February at 4.39%, up from 4.17%. The Bloomberg U.S. Aggregate Bond Index returned -1.41%. The Bloomberg Municipal Bond Index was positive with 0.13%.

The Smart Investor

The late winter holidays are over, and Spring is clearly on the way. With the return of longer days, it may seem easier to get more done. As you start to think about Spring cleaning, have you given any thought to your financial housekeeping?

· Tax season is upon us. As you go through the process, have you identified steps you could take to lower your taxes next year? Don’t put those off. Maximizing a 401(k) is easier if you start early, and adding every month, instead of all at once, can lower your risk.

· There’s still time to lock in high CD rates. Have you thought about putting your cash to work?

· Is your emergency fund keeping up with your lifestyle and your income? Time to tune it up

· Are you missing anything? This phase of the cycle is still in flux, but rates are likely to be higher, and volatility may be spiky. Is your portfolio diversified enough to cushion any shocks?

Keeping your finances on track with your goals is something you don’t want to think about all the time, but focusing on it can ensure you create the flexibility you want throughout your financial journey. If you have questions, we’re always here to help.